For most people, there is no change in the actual tax rate, rebate amount, or deadline for filing returns under the New Income Tax Act 2025. It is only in relation to structure, numbering, terminology, and a few other sections where there has been any alteration.

Feature | Status Under ITA 2025 |

| Income Tax Rates (New Regime) | Unchanged |

| Income Tax Rates (Old Regime) | Unchanged |

| Deduction Limits (80C Equivalent) | Unchanged – ₹1.5 lakh |

| Section 87A Rebate | Unchanged – ₹60,000 up to ₹12 lakh income |

| Standard Deduction | Unchanged – ₹75,000 for salaried taxpayers |

| Advance Tax Schedule | Unchanged |

| Capital Gains Holding Periods | Unchanged |

| STCG on Equity | Unchanged – 20% |

| LTCG on Equity | Unchanged – 12.5% above ₹1.25 lakh |

| ITR Filing Deadline | Unchanged – 31 July for most individuals |

| Previous Court Judgments | Continue to Apply |

The major difference lies in the formatting of the new act itself. Under the new Income Tax Act 2025, there will be new section numbers, new terminologies, new forms, and a few new sections, including one on share buyback, HRA cities, and children’s education allowance.

The New Income Tax Act 2025 does not become applicable immediately for filing tax returns. Your tax return will be governed by a law based on the financial year in which you are filing your taxes.

Income Earned In | Return Filing Period | Governing Act |

| FY 2025–26 (Apr 2025 to Mar 2026) | July 2026 (AY 2026–27) | Income Tax Act, 1961 |

| Tax Year 2026–27 (Apr 2026 to Mar 2027) | July 2027 | New Income Tax Act, 2025 |

| FY 2024–25 and Earlier | Filed or Pending | Income Tax Act, 1961 |

For example, if you file an income tax return in July 2026 for the financial year 2025-26, then the Income Tax Act, 1961 will still be governing. All the existing sections such as 80C, 80D, 115BAC, and 194J will also apply. Furthermore, existing forms such as Forms 16, 16A, and Forms 15G/15H will also be valid.

The applicability of the New Income Tax Act 2025 will start after the financial year commencing April 2026. This means that the first income tax return filing will likely be filed in July 2027.

One of the significant amendments in the New Income Tax Act 2025 is the concept of ‘Tax Year,’ which takes over the usage of ‘Previous Year’ and ‘Assessment Year.’

In the Income Tax Act, 1961, taxpayers were required to apply two concepts: “Previous Year,” relating to the year when income is earned, and “Assessment Year,” referring to the year when the tax return is submitted. In the current tax act, there is only one concept of ‘Tax Year’ that refers to the fiscal year in question.

For instance, Tax Year 2026–27 means income earned during April 2026 through March 2027, with the tax return being submitted in July 2027. If you file your tax return in July 2026 for FY 2025–26, you will continue using the former concept.

In terms of provisions under the New Income Tax Act 2025, the sections have undergone a full re-numbering process. Even though the tax provisions themselves remain essentially the same, taxpayers must get used to the changed numbering system of sections.

What It Covers | Income Tax Act, 1961 | Income Tax Act, 2025 |

| 80C Investments (PPF, ELSS, PF) | Section 80C | Section 150 |

| Health Insurance Premium | Section 80D | Section 151 |

| New Tax Regime | Section 115BAC | Section 202 |

| TDS on Salary | Section 192 | Section 392 |

| TDS on Non-Salary Payments | Sections 193–194T | Section 393 |

| Tax Collected at Source (TCS) | Section 206C | Section 394 |

| Self-Assessment Tax | Section 140A | Section 309 |

| Return of Income | Section 139 | Section 263 |

| Tax Audit | Section 44AB | Section 63 |

| Search and Seizure | Section 132 | Section 247 |

Re-numbering is among the most prominent differences, although it does not affect taxation itself. The taxpayers who file their returns in July 2026 for FY 2025-26 would use the previous numbering system, such as Sections 80C, 80D, and 115BAC. These newly numbered sections will become applicable for return filing starting July 2027.

The New Income Tax Act 2025 also includes the introduction of new form numbers, though the use of most of the forms is similar to before.

Old Form (Income Tax Act, 1961) | New Form (Income Tax Act, 2025) | Effective From |

| Form 16 (Salary TDS Certificate) | Form 130 | June 2027 |

| Form 16A (Non-Salary TDS Certificate) | Form 131 | June 2027 |

| Form 15G | Form 121 | FY 2026–27 |

| Form 15H | Form 121 | FY 2026–27 |

| Form 3CD (Tax Audit Report) | Form 26 | Tax Year 2026–27 |

Form 15G and Form 15H will be replaced by one single form called Form 121. In a similar manner, the names Form 16 and Form 16A will be changed to Form 130 and Form 131 respectively.

If you file your income tax returns in July 2026 for the fiscal year 2025-26, there are no differences at all. Your employer will continue issuing Form 16, and all forms will retain their existing name until June 2027.

The TDS provisions in the Income Tax Act 1961 had been scattered over many sections. The new income tax act 2025 has made things easy for businesses by concentrating TDS rules into two major sections—Section 392 for TDS from salary and Section 393 for TDS on all other than salary payments.

Nothing will change for business regarding the rate, threshold, and compliance rules. Business entities just have to make amendments in their software after Tax Year 2026-27.

While most tax rules remain the same, the New Income Tax Act 2025 introduces a few substantive changes that can directly affect taxpayers and investors.

The tax treatment of share buyback proceeds has changed from dividend taxation to capital gains taxation. This may result in more favourable treatment for many retail investors, while promoters and promoter-held entities may face specified tax rates under the new framework.

The 50% HRA exemption category under the old tax regime, previously limited to Delhi, Mumbai, Kolkata, and Chennai, is proposed to include Bengaluru, Pune, Hyderabad, and Ahmedabad. Employees in these cities may be able to claim a higher HRA exemption.

The exemption limit for children’s education allowance is proposed to increase significantly, offering a higher deduction under the old tax regime for eligible taxpayers with school-going children.

PAN quoting requirements are being streamlined to focus on high-value and higher-risk transactions while reducing compliance for smaller routine transactions.

From April 2026, the income tax e-filing portal is expected to display two separate tabs to help taxpayers file returns under the correct law.

If you are filing your return in July 2026 for income earned during FY 2025–26, you should continue to use the Income Tax Act, 1961 tab. The new tab under the Income Tax Act, 2025 will apply only to returns filed for income earned from April 2026 onward.

For most taxpayers, the New Income Tax Act 2025 does not change the core rules used to calculate and file income tax. The following provisions continue to remain the same.

In short, while the law has been reorganized and renumbered, the basic tax rules and benefits that most individuals rely on remain unchanged.

The transition to the New Income Tax Act 2025 may create confusion around section numbers, form names, and the correct law for each filing year.

TaxBiz has helped over 5 million Indians file income tax returns accurately. Our ICAI-registered CAs ensure your return is filed under the correct Act with the right forms and provisions.

Is your salary income more than INR 20 lakhs? Do you feel the pinch of higher...

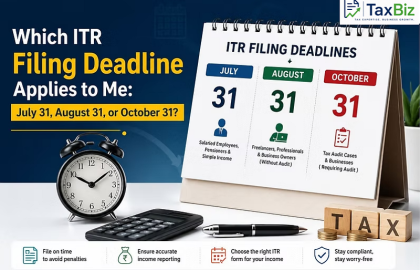

ITR filing deadlines for FY 2025–26 (AY 2026–27) are no longer the same for every taxpayer....