We will take you through essential tips, from how to use the deductions under the appropriate Sections of the Income Tax Act to making wise investment decisions so that you not only remain compliant with the tax laws but also get the best value for your hard-earned money. Let's get into the details on how to keep more of your salary above 20 lakhs in your pocket.

The tax system in India is designed into brackets, meaning that as the income rises, so does the tax rate. For individuals whose income exceeds 20 lakhs, the applicable tax rate also increases, so their income falls under a higher tax slab. More specifically, the tax rate is 30% for the income slab above 10 lakhs up to 50 lakhs. This rate is exclusive of the health and education cess of 4% and any applicable surcharge, which is 10% for income between 50 lakhs and 1 crore.

Impact of Crossing the 20 Lakh Threshold on Your Tax Liabilities: Crossing the 20 lakh income threshold significantly increases your tax liabilities. You move from a 20% to a 30% tax slab for your income exceeding 10 lakhs. This transition means that every incremental income earned above that limit is now taxed at a higher rate, thus increasing your overall tax burden. Efficient tax planning becomes crucial to minimize this liability through legal channels and smart investments.

It is very important that you avail all the possible deductions under the Income Tax Act to bring down the taxable income to the best possible extent. Here's how you can avail yourself of some key sections:

Section 80C allows for a deduction of up to INR 1.5 lakhs from your taxable income. You can manage to get this if you invest in Public Provident Fund (PPF), National Savings Certificates (NSC), Equity-Linked Savings Scheme (ELSS), and others. These investments will not only cut your tax down but will also help you save money and ensure your financial security.

Under Section 80D, the premium paid on health insurance for self and family is allowed for deductions. The limit for deduction is INR 25,000 for individuals below 60 years, which can increase to INR 50,000 if the insurance covers senior citizens. The deduction is over and above the limits allowed under Section 80C.

If you have taken an education loan, the interest that you pay on that loan is deductible under Section 80E. It is available for a maximum period of 8 years or till the interest is paid, whichever is earlier. There is no limit on the amount which can be claimed under this section. It is, therefore, a very valuable option in reducing the tax base, especially for high-income earners supporting higher education for themselves or their children.

In addition to the basic deductions under the Income Tax Act, there are several other sections that provide opportunities to further reduce your taxable income. Here's a detailed look at some of these sections which can be particularly beneficial for those with a salary above 20 lakhs:

National Pension System (NPS): An additional deduction of up to INR 50,000 is available under Section 80CCD(1B) for investments made in the NPS. This is over and above the deduction of INR 1.5 lakh available under Section 80C. NPS is a government-sponsored pension scheme that not only helps in tax saving but also secures your retirement with a steady pension.

Home Loan Interest: If you have a home loan, the interest paid on the loan can be claimed as a deduction under Section 24. The limit for this deduction is up to INR 2 lakh per annum for a self-occupied property. There is no upper limit for the deduction on rental properties, but the loss under the head of house property that can be set off against other heads of income is restricted to INR 2 lakh per annum. This deduction can significantly reduce your taxable income, especially if you are in the higher income bracket.

Rent Paid: For those who do not receive House Rent Allowance (HRA) as part of their salary and are paying rent, Section 80GG offers a deduction. The deduction allowed is the least of the following:

To claim this deduction, you must not own any residential accommodation at the place where you currently reside, perform office duties, or carry on business or profession.

By strategically planning and utilizing these additional deductions, individuals earning above 20 lakhs can effectively reduce their taxable income. It’s important to:

Invest wisely in schemes like NPS which provide long-term benefits along with tax savings.

Consider the tax implications when deciding on buying versus renting a home, especially if you have the option of claiming significant deductions on home loan interest.

Maintain proper documentation and receipts for rent payments and investments to substantiate claims during tax filing.

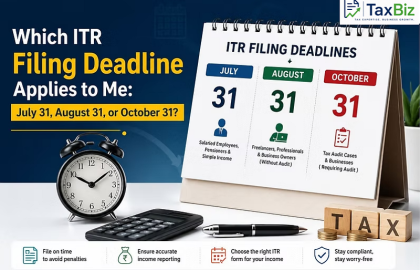

ITR filing deadlines for FY 2025–26 (AY 2026–27) are no longer the same for every taxpayer....

The tax system of India is currently undergoing restructuring under the New Income Tax Act 2025....